用LSTM预测股票行情

这里采用沪深300指数数据,时间跨度为2010-10-10至今,选择每天最高价格。假设当天最高价依赖当天的前n(如30)天的沪深300的最高价。用LSTM模型来捕捉最高价的时序信息,通过训练模型,使之学会用前n天的最高价,判断当天的最高价(作为训练的标签值)。

导入数据

这里使用tushare来下载沪深300指数数据。可以用pip 安装tushare。

import tushare as ts #导入cons = ts.get_apis() #建立连接#获取沪深指数(000300)的信息,包括交易日期(datetime)、开盘价(open)、收盘价(close),#最高价(high)、最低价(low)、成交量(vol)、成交金额(amount)、涨跌幅(p_change)df = ts.bar('000300', conn=cons, asset='INDEX', start_date='2010-01-01', end_date='')#删除有null值的行df = df.dropna()#把df保存到当前目录下的sh300.csv文件中,以便后续使用df.to_csv('sh300.csv')本接口即将停止更新,请尽快使用Pro版接口:https://waditu.com/document/2

数据概览

(1)查看下载数据的字段、统计信息等。

#查看df涉及的列名print(df.columns)# Index(['code', 'open', 'close', 'high', 'low', 'vol', 'amount', 'p_change'], #dtype='object')#查看df的统计信息df.describe()Index(['code', 'open', 'close', 'high', 'low', 'vol', 'amount', 'p_change'], dtype='object')

| open | close | high | low | vol | amount | p_change | |

|---|---|---|---|---|---|---|---|

| count | 2795.000000 | 2795.000000 | 2795.000000 | 2795.000000 | 2.795000e+03 | 2.795000e+03 | 2795.000000 |

| mean | 3342.024819 | 3344.784845 | 3370.611827 | 3314.019947 | 1.146134e+06 | 1.499518e+11 | 0.023324 |

| std | 809.944990 | 810.070118 | 816.521375 | 800.923783 | 8.775841e+05 | 1.306605e+11 | 1.448982 |

| min | 2079.870000 | 2086.970000 | 2118.790000 | 2023.170000 | 2.190120e+05 | 2.120044e+10 | -8.750000 |

| 25% | 2618.540000 | 2620.265000 | 2645.770000 | 2598.400000 | 6.107925e+05 | 6.605147e+10 | -0.640000 |

| 50% | 3292.280000 | 3293.870000 | 3315.730000 | 3258.310000 | 8.908120e+05 | 1.074772e+11 | 0.040000 |

| 75% | 3836.075000 | 3837.775000 | 3859.115000 | 3813.550000 | 1.344036e+06 | 1.847992e+11 | 0.720000 |

| max | 5922.070000 | 5807.720000 | 5930.910000 | 5747.660000 | 6.864391e+06 | 9.494980e+11 | 6.710000 |

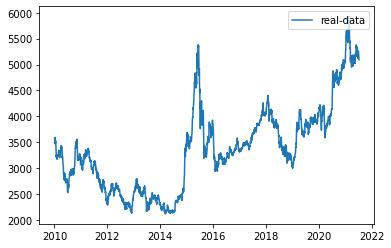

(2)可视化最高价数据

import numpy as npdf_index=df.codedf_index = df_index.index.tolist()# df_index=[str(year)[0:4] for year in df_index]df_all = np.array(df['high'].tolist())df=df['high']from pandas.plotting import register_matplotlib_convertersimport matplotlib.pyplot as pltregister_matplotlib_converters()# 获取训练数据、原始数据、索引等信息df, df_all, df_index = readData('high')#可视化最高价df_all = np.array(df_all.tolist())plt.plot(df_index, df_all, label='real-data')plt.legend(loc='upper right')<matplotlib.legend.Legend at 0x7fc8a932bfa0>

预处理数据

import pandas as pdimport matplotlib.pyplot as pltimport datetimeimport torchimport torch.nn as nnimport numpy as npfrom torch.utils.data import Dataset, DataLoaderimport torchvisionimport torchvision.transforms as transforms%matplotlib inline

(1)生成训练数据

#通过一个序列来生成一个31*(count(*)-train_end)矩阵(用于处理时序的数据)#其中最后一列维标签数据。就是把当天的前n天作为参数,当天的数据作为labeldef generate_data_by_n_days(series, n, index=False): if len(series) <= n: raise Exception("The Length of series is %d, while affect by (n=%d)." % (len(series), n)) df = pd.DataFrame() for i in range(n): df['c%d' % i] = series.tolist()[i:-(n - i)] df['y'] = series.tolist()[n:] if index: df.index = series.index[n:] return df #参数n与上相同。train_end表示的是后面多少个数据作为测试集。def readData(column='high', n=30, all_too=True, index=False, train_end=-500): df = pd.read_csv("sh300.csv", index_col=0) #以日期为索引 df.index = list(map(lambda x: datetime.datetime.strptime(x, "%Y-%m-%d"), df.index)) #获取每天的最高价 df_column = df[column].copy() #拆分为训练集和测试集 df_column_train, df_column_test = df_column[:train_end], df_column[train_end - n:] #生成训练数据 df_generate_train = generate_data_by_n_days(df_column_train, n, index=index) if all_too: return df_generate_train, df_column, df.index.tolist() return df_generate_train

模型

(1)定义模型

class RNN(nn.Module): def __init__(self, input_size): super(RNN, self).__init__() self.rnn = nn.LSTM( input_size=input_size, hidden_size=64, num_layers=1, batch_first=True ) self.out = nn.Sequential( nn.Linear(64, 1) ) def forward(self, x): r_out, (h_n, h_c) = self.rnn(x, None) #None即隐层状态用0初始化 out = self.out(r_out) return outclass mytrainset(Dataset): def __init__(self, data): self.data, self.label = data[:, :-1].float(), data[:, -1].float() def __getitem__(self, index): return self.data[index], self.label[index] def __len__(self): return len(self.data)(2)超参数设置n = 30LR = 0.001EPOCH = 200batch_size=20train_end =-600device = torch.device('cuda' if torch.cuda.is_available() else 'cpu')

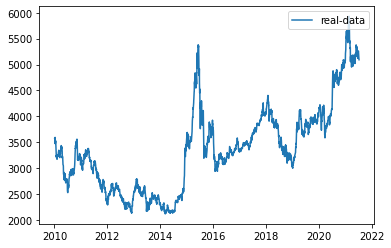

(3)训练模型

from pandas.plotting import register_matplotlib_convertersregister_matplotlib_converters()# 获取训练数据、原始数据、索引等信息df, df_all, df_index = readData('high', n=n, train_end=train_end)#可视化原高价数据df_all = np.array(df_all.tolist())plt.plot(df_index, df_all, label='real-data')plt.legend(loc='upper right') #对数据进行预处理,规范化及转换为Tensordf_numpy = np.array(df)df_numpy_mean = np.mean(df_numpy)df_numpy_std = np.std(df_numpy)df_numpy = (df_numpy - df_numpy_mean) / df_numpy_stddf_tensor = torch.Tensor(df_numpy)trainset = mytrainset(df_tensor)trainloader = DataLoader(trainset, batch_size=batch_size, shuffle=False)

#记录损失值,并用tensorboardx在web上展示from tensorboardX import SummaryWriterwriter = SummaryWriter(log_dir='logs')rnn = RNN(n).to(device)optimizer = torch.optim.Adam(rnn.parameters(), lr=LR)loss_func = nn.MSELoss()for step in range(EPOCH):for tx, ty in trainloader:tx=tx.to(device)ty=ty.to(device)#在第1个维度上添加一个维度为1的维度,形状变为[batch,seq_len,input_size]output = rnn(torch.unsqueeze(tx, dim=1)).to(device)loss = loss_func(torch.squeeze(output), ty)optimizer.zero_grad()loss.backward()optimizer.step()writer.add_scalar('sh300_loss', loss, step)

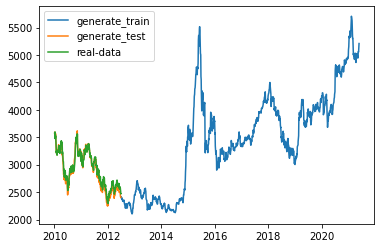

(4)测试模型

generate_data_train = []generate_data_test = []test_index = len(df_all) + train_enddf_all_normal = (df_all - df_numpy_mean) / df_numpy_stddf_all_normal_tensor = torch.Tensor(df_all_normal)for i in range(n, len(df_all)):x = df_all_normal_tensor[i - n:i].to(device)#rnn的输入必须是3维,故需添加两个1维的维度,最后成为[1,1,input_size]x = torch.unsqueeze(torch.unsqueeze(x, dim=0), dim=0)y = rnn(x).to(device)if i < test_index:generate_data_train.append(torch.squeeze(y).detach().cpu().numpy() * df_numpy_std + df_numpy_mean)else:generate_data_test.append(torch.squeeze(y).detach().cpu().numpy() * df_numpy_std + df_numpy_mean)plt.plot(df_index[n:train_end], generate_data_train, label='generate_train')plt.plot(df_index[train_end:], generate_data_test, label='generate_test')plt.plot(df_index[train_end:], df_all[train_end:], label='real-data')plt.legend()plt.show()

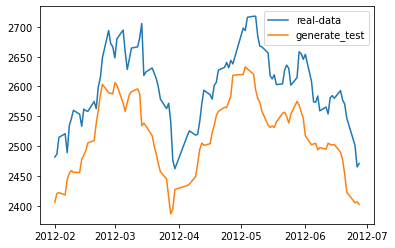

plt.clf()plt.plot(df_index[train_end:-500], df_all[train_end:-500], label='real-data')plt.plot(df_index[train_end:-500], generate_data_test[-600:-500], label='generate_test')plt.legend()plt.show()

")

浅谈控制反转(IOC)与依赖注入(DI)")

还没有评论,来说两句吧...